Four decades ago, in the mid-1970s, young American adults--in the 18-to-34 age bracket--were far more likely to be married and living with a spouse than living in their parents’ home.

“There are now more young people living with their parents than in any other arrangement,” says the Census Bureau study.

“What is more,” says the study, “almost 9 in 10 young people who were living in their parents’ home a year ago are still living there today, making it the most stable living arrangement.”

The Number 1 living arrangement today for Americans in the 18-to-34 age bracket, according to the Census Bureau, is to reside without a spouse in their parents’ home.

That is where you can now find 22.9 million 18-to-34 year olds—compared to the 19.9 million who are married and live with their spouse.

In 1975, according to Census Bureau data, 31.9 million Americans in the 18-to-34 age bracket were married and lived with their spouse.

Back then, this was the most common living arrangement for that age bracket.

Also in 1975, 14.7 million in the 18-to-34 age bracket lived in their parents’ home; 6.1 million lived in an “other” arrangement (including with siblings, grandparents, other relatives, or unrelated roommates); 3.1 million lived alone, and 0.7 million cohabitated with an unmarried partner.

In 2016, according to the Census Bureau, only 19.9 million were married and lived with a spouse—while 22.9 million lived in their parents’ home.

Also in 2016, 15.6 million lived in an “other” arrangement. 9.2 million cohabitated with an unmarried partner, and 5.9 million lived alone.

The Census Bureau counted college students living in a dormitory as living in their parents' home. By contrast, it counted someone as living with a spouse even if they and their spouse still lived with a parent. The category of living with a spouse, the study said, included any “young adult who lives with a spouse, regardless of whether anyone else is present in the household (e.g., parents, roommates, other family members).”

In 1975, when calculated as percentages according to the Census numbers, 57 percent of 18-to-34 year olds lived with a spouse, 26 percent lived in their parents’ home, 11 percent lived in an “other” arrangement, 5 percent lived alone, and 1 percent lived with an unmarried partner.

In 2016, 31 percent lived in their parents’ home, 27 percent lived with their spouse, 21 percent lived in an “other” arrangement, 12 percent lived with an unmarried partner, and 8 percent lived alone.

The rise in young adults living at home coincided with a decline in the economic status of young men.

“More young men are falling to the bottom of the income ladder,” says the Census Bureau study. “In 1975, only 25 percent of men, aged 25 to 34, had incomes of less than $30,000 per year. By 2016, that share rose to 41 percent of young men (incomes for both years are in 2015 dollars).”

“There are now more young women than young men with a college degree, whereas in 1975 educational attainment among young men outpaced that of women,” says the study.

In the last decade, says the study, the pace of change in the living arrangements of young Americans has been rapid--but has not been uniform across the states and regions of the country.

“Within the last 10 years, the breadth and speed of change in living arrangements have been tremendous,” it says. “In 2005, the majority of young people lived independently in their own household (either alone, with a spouse, or an unmarried partner), which was the predominant living arrangement in 35 states. By 2015—just a decade later—only six states had a majority of young people living independently.”

With the exceptions of California and Mississippi, the Top Ten states with the highest percentages of 18-to-34 year olds living with their parents were concentrated along the Atlantic coast. (See chart below). They included: New Jersey (46.9%), Connecticut (41.6%), New York (40.6%) Maryland (38.5%), Florida (38.3%), California (38.1%), Rhode Island (37.1%), Pennsylvania (37.1%), Massachusetts (37.0%) and Mississippi (36.8%).

With the exceptions of Washington and Oregon, the ten states with the lowest percentages of 18-to-34 year olds living with their parents were concentrated in the Midwest and Mountain states.

These included North Dakota (14.1%), South Dakota (19.9%), Wyoming (20.9%), Nebraska (22.7%), Iowa (22.8%), Montana (24.1%), Colorado (24.6%), Kansas (26.0%), Washington (26.6%) and Oklahoma (26.7%), which tied with Oregon (26.7%).

“Why are there geographical differences in young adult living arrangements?” the Census study asks. “For one, local labor and housing markets shape the ability of young people to find good jobs and affordable housing, which in turn affects whether and when they form their own households.”

Congratulations America! You've become Mexico, and most other 3rd World Nations!!!! You've finally made it to the 18th Century, with 21st Century technology!!!

Libertatem Prius!

To view links or images in signatures your post count must be 15 or greater. You currently have 0 posts.

Puerto Rico's governor on Wednesday announced a historic restructuring of a portion of the U.S. territory's $70 billion debt through courts after negotiations with bondholders failed. The announcement marks the biggest bankruptcy-type process ever for the U.S. municipal bond market.

Gov. Ricardo Rossello said that a federal control board overseeing the island's finances agreed with his request late Tuesday to put certain debts before a court.

"We're going to protect our people," he said hours after the U.S. territory was hit with multiple lawsuits from creditors seeking to recuperate the millions of dollars they invested in bonds issued by Puerto Rico's government, which has declared several defaults amid a 10-year recession.

Rossello said one of the lawsuits sought to claim all revenues generated by the island's Treasury Department for bondholders.

"I'm not going to allow that to happen," he said.

Rossello said the debts of certain agencies will be restructured in court, while others will be resolved through ongoing negotiations with bondholders. He said he did not yet have details on the breakdown of those debts. The island's Electric Power Authority has some $9 billion of debt, the Aqueducts and Sewer Authority has roughly $5 billion of debt and the Highways and Transportation Authority has around $7 billion of debt.

A federal district court judge will now be in charge of the restructuring. Bondholders cannot challenge Rossello's decision until 120 days from now.

Elias Sanchez, the governor's representative to the board, criticized creditors for filing lawsuits even as the governor continued to hold what he called good-faith negotiations after a litigation freeze expired after May 1.

"When a line is crossed, the government has to act in favor of the people of Puerto Rico."

Several groups representing bondholders did not immediately return requests for comment.

In the next couple of days, the chief justice of the U.S. Supreme Court is expected to appoint a federal district court judge to oversee Puerto Rico's case, he said. Meanwhile, the government will continue to talk to creditors and seek a stay on the nearly two dozen lawsuits that the U.S. territory faces.

Sanchez noted that unlike a regular bankruptcy in the U.S. mainland, a judge cannot unilaterally seize any of Puerto Rico's assets and turn them over to bondholders.

"The courts cannot say, 'We're going to give you the Puerto Rico coliseum, or these properties from the Land Authority," he said. "They just cannot do that without the consent of the board."

Puerto Rico is facing $70 billion in debt. By comparison, the U.S. city of Detroit had $9.3 billion of obligations when it filed for bankruptcy in 2013 in the biggest U.S. municipal bankruptcy ever.

While Detroit's case was resolved in a couple of years, it is unclear how long it will take for Puerto Rico.

"This is much bigger and much more complex than Detroit," Sanchez said, adding that he estimates the process could be completed within four years.

The announcement has sparked widespread uncertainty on the island, where Puerto Ricans are struggling with increases in taxes, higher utility rates and an unemployment rate that has hovered around 12 percent. The crisis has prompted nearly 450,000 Puerto Ricans to leave the island for the U.S. mainland in the past decade.

It is too early to say what kind of impact a debt restructuring in court will have on the 3.4 million people that remain on the island, economist Jose Joaquin Villamil told The Associated Press.

"(It) presents a very big risk for both parties," he said, referring to the government and to bondholders. "We don't know what a federal district court judge is going to decide."

However, he warned that the process will further spook the type of investors that Puerto Rico's economy needs as it prepares to implement several austerity measures. Sanchez disputed that opinion, saying that a court-supervised restructuring would actually provide more comfort to investors.

Economist Gustavo Velez told the AP that Rossello's announcement is the best path for Puerto Rico at this point. The previous governor announced that the $70 billion debt load was unpayable and needed restructuring.

"It's been three years of agony, uncertainty and negotiations that have cost the island millions in consultants that have produced no results," he said. "We cannot keep stretching this chewing gum further."

The United States has enjoyed extraordinary economic progress over the past four decades, but average incomes for today's young workers are lower than they were in 1975.

Over the past four decades, young American workers saw their average incomes decline by 5.5 percent after adjusting for inflation, according to new figures published Wednesday by the U.S. Census Bureau. In 1975, workers aged 25 to 34 had a median personal income of $37,000 in modern dollar terms. In 2016, that number was down to $35,000.

Earnings have declined despite the fact that today's young people are better educated than 40 years ago. Thirty-seven percent of young people had a bachelor's degree last year, compared to 22.8 percent in 1975.

In part, experts say, the decline in average incomes results from new impediments to financial success that confront millennials, but that older Americans did not have to overcome. A more unequal economy presents fewer opportunities for younger workers. Young people today must compete with a well educated labor force, while young people in the past often had an advantage over older workers who were less qualified.

In another sense, the decline represents progress, because it is partly a result of striking gains among young women. Young women have joined the workforce in high numbers, but because they still earn less than young men, their entrance has driven down the average for young workers in general. In 1975, just under half of women aged 25 to 34 were working, and only 18.4 percent had at least a bachelor's degree. In 2016, about 70 percent of women between those ages were employed, and 40 percent had at least a bachelor's degree.

The typical income for a young woman in the labor force increased 28.5 percent since 1975, from $23,000 to $29,000 in 2015 dollars.

Meanwhile, young men's earnings have declined. For a man in the labor force aged 25 to 34, the typical income declined from $46,000 in 1975 to $40,000 last year.

Young men are also more educated — 34 percent now have a bachelor's degree, compared to 27.4 percent of their counterparts 40 years ago. Last year, roughly 5 in 6 were working and two-thirds had full-time, year-round jobs, figures that have changed little since 1975.

“It’s hard to say that there’s one experience for young adults that’s capturing how they’re all doing,” said the Census's Jonathan Vespa, the author of the report.

The stagnant fortunes of young people comes amid broad overall gains for the American since 1975. Median personal income for all Americans has increased from about $23,000 in 1975 to $30,000 today in 2015 dollars. (Those figures include many retirees and students.)

Data from the Bureau of Labor Statistics on those with full-time, year-round work confirms the negative trend for the young. Typical weekly earnings for workers aged 25 to 34 in this category have declined 4 percent between 1979 and last year after adjusting for inflation, according to Arloc Sherman, a researcher at the liberal Center on Budget and Policy Priorities.

Gary Burtless, an economist at the nonpartisan Brookings Institution, suggested a few explanations for the disappointing data for young people. The level of education in the American labor force was rapidly increasing in 1975. While it was typical for older workers at that time not to have completed high school, a new generation — the baby boomers — had received what Americans now think of as a standard education, including a high-school diploma and increasingly a bachelor's degree.

As a result, young people could claim more of the fruits of the American economy then. “Compared to older workers, back then, they at least had a couple of very strong advantages,” Burtless said. “Those advantages are smaller for young adults today.”

At the same time, he said, inequality of income has increased in general in the American economy, meaning that poorer workers — many of whom are younger — have not enjoyed the same progress as more affluent workers, who tend to be older.

“It’s a big problem, even for people with college credentials,” he said. “Those less educated people have fared quite miserably.”

50% are woefully unprepared for a financial emergency.

Nearly 1 in 5 (19%) Americans have nothing set aside to cover an unexpected emergency.

Nearly 1 in 3 (31%) Americans don’t have at least $500 set aside to cover an unexpected emergency expense, according to a survey released Tuesday by HomeServe USA, a home repair service.

A separate survey released Monday by insurance company MetLife found that 49% of employees are “concerned, anxious or fearful about their current financial well-being.”

The Federal Reserve announced Friday that the U.S. has $1 trillion in credit-card debt. Consumers hit that number in the fourth quarter of 2016, but eased on revolving credit during January 2017. The Fed announcement showed revolving consumer credit hit more than $1 trillion once again in February 2017.

“Credit card debt is rising quickly, but delinquencies are still really low,” said Matt Schulz, a senior industry analyst at the credit cards site CreditCards.com. “Many Americans are doing a good job of controlling their debts, but eventually with big debts and rising interest rates, it’s likely that something will have to give.”

Paycheck to Paycheck “Good Job”

Excuse me for asking but if half the nation lives paycheck to paycheck, is that really indicative of doing a good job at managing debt.

The stock market and housing are still going strong. We heard the same thing in 2007 but it’s different this time.

The bottom 50% of the economy simply do not matter.

The real crux of the matter is point number two.

The Fed does not give a damn about the bottom half of the economy even though it spouts continual lies about “income inequality.

The Bottom 50% Do Not Matter

As long as the Fed can keep stocks and home prices elevated, there is no concern about the food-stamp, rent-subsidized, Medicaid-supplement, disability-income, Obamacare-subsidized 50% of Americans struggling paycheck-to-paycheck.

That money rolls in guaranteed, month after month!

That 50% cannot afford a house is irrelevant as long as suckers keep paying $500,000 to two-bedroom shacks in LA.

The game is to keep asset prices up so that the top 50% keep spending. The bottom 50% are taken care of by government (taxpayer) subsidies noted above.

Here’s something Wal-Mart could do to Amazon, just to be nasty.

Amazon expects to slash jobs and other costs at Whole Foods, “a person with knowledge of the company’s grocery plans” told Bloomberg. The ink isn’t even dry on the proposed deal, but synergies and efficiencies are already being trotted out.

Amazon agreed to acquire Whole Foods for $13.7 billion, a 27% premium over the stock price on Thursday at close, and now intends to push down prices to slough off Whole Food’s nickname “Whole Paycheck,” and go after Wal-Mart Stores, Target, the German discounters Aldi and Lidl that are expanding in the US, Costco, and grocery store chains, such as Kroger and the private-equity owned chains Safeway and Albertson’s.

The jobs to be cut include cashiers, who’d be replaced by Amazon’s own “Just Walk Out Technology,” now being tested at its Amazon Go convenience store in Seattle. When customers with the Amazon Go app on their smartphones walk into the store, the system logs them into the store’s network and establishes the connection to their Amazon account.

The system uses “computer vision, sensor fusion, and deep learning,” Amazon says, to track everything customers pull off the shelf. If customers put an item back, the system removes it from the virtual cart in their app. When done, customers can just walk out without having to go through a check-out line. The system will automatically charge the customer’s account and send out a receipt.

This system would replace the cashiers at Whole Foods, “according to the person familiar with the matter, who asked not to be named because the plans are private,” Bloomberg reported.

So not the cumbersome self-check-out machines we’ve been grappling with for years, but something that would allow Amazon to differentiate itself. However, the main advantage would be a radical reduction in labor costs at Whole Foods stores. The “employees remaining would help improve the shopping experience, the person said,” according to Bloomberg.

Amazon also expects to make a number of other changes, including to the merchandise the store carries, all in order to push down prices. Amazon would introduce private-label products – in addition to Whole Foods’ existing private-label products – to replace products that it considers too expensive. So get ready for Amazon’s food brands.

These changes won’t take place until after the transaction has closed, which is expected to be later this year.

The grocery price war is already red-hot. So the high prices that have hobbled Whole Foods over the past two years will likely be gone.

After Whole Foods becomes part of the Amazon empire later this year, it no longer needs to make significant and growing profits. That quaint concept is out the window.

Amazon is like so beyond that. It can lose money, no problem. On its own, Whole Foods could have never done that.

An Amazon spokesperson denied everything. Amazon has “no plans to use no-checkout technology to automate the jobs of cashiers at Whole Foods and no job reductions are planned,” he told Bloomberg in a statement.

Alas, almost all acquisitions of this type entail efforts to find synergies and efficiencies, as they’re called, to bring costs down to make the transaction work, which translates into hefty job cuts. And since the deal is far from closing, there need not be official “plans” at this point.

Amazon has made an art out of pricing, with prices jumping up and down dramatically, depending on who is looking at it, what kinds of cookies and browsing history they have on their devices, and what is known about them, for example when they’re checking a price while logged into Amazon.

This “variable pricing” model – which has spawned an entire sub-industry to defeat it – has spread to other retailers and can drive astute shoppers nuts. Of course, airlines and other industries also have used it for years. It would be interesting to see if Amazon can figure out how to move it to its brick-and-mortar stores – say, with prices only being posted on smartphones with the Amazon Go app when you get to the product.

Amazon is also going after low- and middle-income shoppers. For a mass-market retailer, it needs all customers. It already has cheaper Amazon Prime memberships for customers who are on government assistance, according to Bloomberg. And it’s testing a program to deliver groceries to recipients of food stamps.

Now if Wal-Mart Stores wanted to put a little squeeze on Amazon, just to be nasty, it could offer something like $4 billion more for Whole Foods so that Amazon would outbid Wal-Mart by offering another $2 billion or $3 billion, at which point Wal-Mart would walk away, celebrating, and Amazon would have to come up with $20 billion to buy Whole Foods, not $13.6 billion, which could dent its credit rating and make things just a little harder for Amazon in the future. Just thinking out loud here.

When Amazon announced the deal, shares of Wal-Mart, Kroger, Costco, and Target get crushed.

Keep up with the new digital age or close the doors.

Creating customer experiences is what matters most.

What retailers can learn from Starbucks.

(Photo credit)

Brick-and-mortar retailers are increasingly losing foot traffic and sales to online retailers as consumers increasingly shift to online shopping, either by desktop or mobile device. Two weeks ago, I argued that traditional retailers need to evolve their stores into one-of-a-kind "destination venues" to create a unique experience for the customer, one that they can't get from an online retailer. Amazon (NASDAQ:AMZN), eBay (NASDAQ:EBAY), Wayfair (NYSE:W), Overstock (NASDAQ:OSTK), just to name a few, are attracting more customers from the Macy's (NYSE:M) of the world.

In-store innovation is crucial, but brick and mortars also need to invest in new technologies to keep up with the new digital age. Macy's, among others, is now re-evaluating their operating models and taking steps to make e-commerce and m-commerce a larger share of their business. Starbucks (NASDAQ:SBUX) has done a great job integrating the mobile experience to enhance customer service and convenience. Mobile order and pay has contributed roughly 25% of the company's U.S. transactions. Retailers can learn a thing or two from the coffee-maker about seamlessly blending the in-store and online shopping experience.

The Amazon Effect

Sears (NASDAQ:SHLD), Macy's, Kohl's (NYSE:KSS), and J.C. Penney (NYSE:JCP) have lost billions of dollars in market value over the past 10 years, mainly because they failed to adapt to a fast-changing retail environment where consumers can easily compare prices and buy things online (see Figure 1).

Retailers like Macy's and Sears stuck with dated and uninspiring store concepts carrying the same merchandise and brands. Less foot traffic and heavy discounting caused sales and profits to plummet. And as a consequence of constant discount-sales events, they lost their pricing power.

Big box retailers forgot about the importance of in-store customer experiences in an omni-channel world. In other words, brick and mortars got too comfortable with what they already had and it bit them. Over the same 10-year period, Amazon's market value has grown by 1,934%.

The so-called "Amazon effect" is driving the way retailers think about their customers, physical stores, and supply chains. Retailers are now rushing to refine their store concepts and online sales strategies to stay relevant and competitive.

Macy's, for example, is streamlining its store portfolio by closing 68 of the planned 100 stores in 2017 and using the cost savings of $250 million to invest in its digital business and other store-related growth strategies.

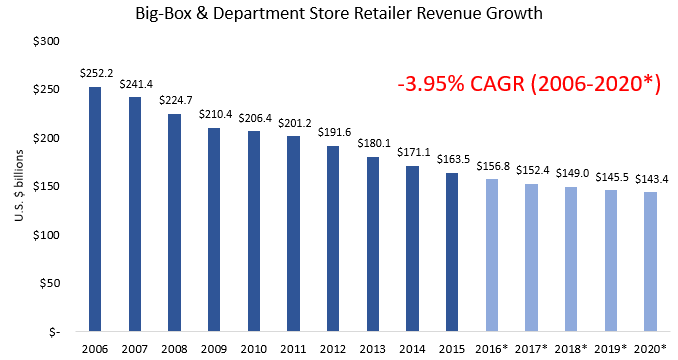

Macy's is taking the right steps to focus on high-growth potential stores and mobile-enabled shopping. But is it too little too late? Not at all if retailers like Macy's make the right investments and adjustments. Big box and department store sales have decreased at a 4.7% compounded annual rate, from 2006 to 2015, according to data from Mazzone & Associates (see Figure 2). I expect the Amazon effect will result in more closures and consolidation in 2017 and 2018 in the broader retail industry.

For instance, Sears is closing 108 Kmart stores and 42 namesake stores in early 2017.

(Figure 2: Retail sales are in a downward spiral. Source: Mazzone & Associates)

Rough Holiday Sales

Brick-and-mortar stores had a rough holiday season. Last week, Macy's and Kohl's both reported a 2.1% drop in November and December comparable store sales and cut their earnings outlook. Weak holiday department store sales reflect the challenges of low retail traffic, off-price retailers, and online shopping.

Mall traffic declined 12.3% in November and December, while mall sales declined 9.9%, according to in-store analytics firm RetailNext.

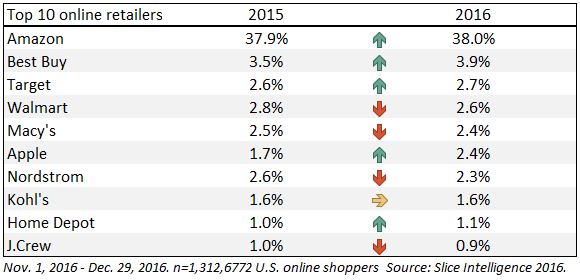

By comparison, Adobe Digital Insights estimates online holiday sales increased 11% to $91.7 billion from a year ago. Of that, Amazon captured nearly 40% of holiday sales in 2016, according to research from Slice Intelligence (see Figure 3). Macy's only claimed 2.4% of all online sales. Overall, the biggest gainer was Apple (NASDAQ:AAPL) collecting 2.4% of sales, up from 1.7% in 2015.

Department store retailers will need to combine the in-store experience and the personalization and convenience of online shopping. Quick service restaurants such as Starbucks have turned to mobile ordering and payment to drive incremental sales, but also to better service customers by learning about their buying habits. And it's working.

Integrating Mobile Tech

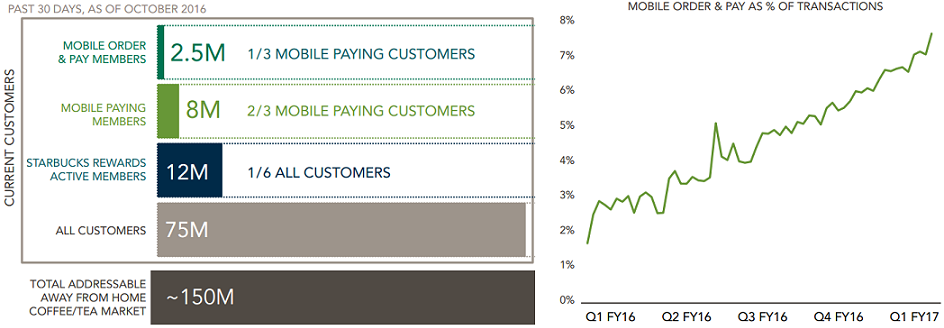

Mobile payments currently account for more than 25% of transactions at Starbucks U.S. operated stores. Starbucks Mobile Order & Pay makes up more than 7% of total U.S. transactions (see Figure 4). Mobile Order & Pay allows customers to customize and place their orders in advance. Pick-up is at a nearby Starbucks store without having to wait in line.

It's quick, easy, and convenient.

(Figure 4: U.S. Starbucks customer breakdown. Starbucks customers are increasingly using Mobile Order & Pay. Source:Starbucks)

As a Starbucks Rewards member, you earn loyalty points or "Stars" with every purchase. You can choose to redeem your Star Reward to get free drinks and food. This reward-based program has encouraged customers to spend more, thus increasing the average transaction and ticket size. Starbucks plans to roll out two new features for the mobile app in 2017 to make food and drink ordering a more personalized service for the customer.

Creative Innovation

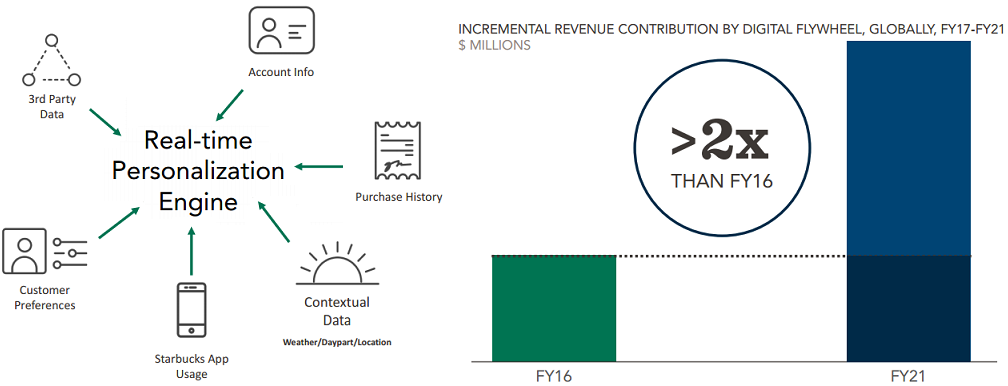

Starbucks is introducing a conversational ordering system called "My Starbucks Barista" which is a digital assistant influenced by Apple's Siri. It will allow customers to place orders via voice command or messaging. The second feature focuses on real-time personalization and product suggestions. Starbucks will track your buying habits and use that information to recommend your favorite food and drinks. This service is specifically tailored to your tastes and preferences (see Figure 5).

(Figure 5: Real-time personalization inside the Starbucks mobile app and revenue growth expectations. Source:Starbucks)

In fiscal 2017, Starbucks expects revenue growth to be driven by mid-single digit comparable sales and the opening of about 2,100 net new stores globally. Last month, Starbucks outlined its five-year plan for global growth. In it, the coffee-maker expects to generate over $35 billion in total revenue and double operating income by fiscal 2021.

Starbucks Mobile Order & Pay will play an important role in achieving these ambitious financial goals. Starbucks expects incremental sales from the digital platform will more than double over the next five years. Starbucks is making the right investments in digital and mobile. These innovative ideas will not only increase sales, but most importantly, increase customer loyalty and experience.

Takeaway

There's a lot that the retail industry can learn from Starbucks' loyalty program and mobile strategy. As mentioned above, the most successful retailers will seamlessly blend their in-store and mobile platforms together to create a unique customer experience. The new digital age is reshaping how people buy things.

Retailers who don't take advantage of these growing technology trends will either continue to see their sales and profits decline, or worse, disappear.

Worried about how to digitally transform while you perform? Wondering how to change the tires while going 60 mph? Are you preparing your team for their digital journey? (It’s not a destination.) Are you trying to figure out how to transform yourself (or your company) into a digital powerhouse in Internet time? All of the above?

The phrase “digital transformation” is so overused that it may be on the brink of its own transformation from a business imperative to a hackneyed refrain. Clichés aside, digital transformation is a business imperative and time is the enemy. So, let’s have a look at seven brain-busting steps that will enable you to create value in your organization through digital transformation.

1. Awareness

Digital transformation requires two kinds of awareness: self-awareness and organizational awareness.

Self-awareness: You must honestly evaluate your personal capabilities. How much did you love or hate math in high school? How much attention did you pay in statistics class in college? Are you a technophobe or a technocrat? Are you excited about learning every day or are you dreading it? These are just a few of the kinds of questions you must honestly answer before you participate in the digital transformation of your world.

You must evaluate your colleagues, subordinates and superiors as well. If you’re not with the right people, it’s exhausting – and that’s putting it mildly.

Organizational awareness: Is it possible for you to digitally transform your group, your unit or ultimately your entire organization? There are several obstacles to digital transformation, and the biggest ones are people-centric such as, a superior who doesn’t believe in digital, or individuals with an entrenched “digital is for kids” belief system, or a “that’s not the way we do it here” mindset.

2. Literacy (not fluency)

You need to be digitally literate. This includes data literacy, coding literacy, machine-learning literacy, math literacy, and question/answering (QA) literacy to name a few. You need not be fluent. As posited in, Data Literacy Will Make You Invincible, “You don’t need to speak French to recognize that the email you just received is written in French. You just need to be literate to the point where you know that Google Translate is not going to get the job done and you need a highly skilled French translator to help you interpret and respond to the communication.”

3. Strategy

Successful digital transformation starts with a solid, well-thought-out strategy that clearly identifies your business objectives. You are going to accomplish _____. Whether it’s cost cutting or media optimization or product design or customer service, have a strategy that identifies a 21st-century problem and proposes a 21st-century solution.

4. Governance

Misalignment of incentives and outcomes is the number one killer of dreams. There is no way that any of your current employees are going to give you an extra minute of their time at the expense of delivering the outcomes they are incentivized (fiscally governed) to deliver. If you’re expecting a unit to make its revenue numbers for the quarter, it should not surprise you to learn that no one in the unit will even do the pre-reading about the new new thing. They’re not getting paid to do it. They won’t profit from it. To effect digital transformation, you must fiscally govern for it.

5. Culture

You must create a culture of innovation where continuous improvement and adaptation to change are constant. While it is difficult to transform a culture of “Always be closing” or “Make your numbers or else,” if you want to digitally transform your organization, you are going to have to do whatever it takes to assemble your orchestra in an environment where the musicians play music, not just notes.

6. Test, Fail, Learn

Failure is not an option; it is a probability. Part of a successful culture of innovation is an iterative process for testing, failing, learning, reworking, and repeating the process. This is far easier to say than to do. It is especially difficult when an “intrepreneur” has sold in a vision, built a business plan and created a roadmap and then is forced to follow the road, not the map. This is where leadership outplays management.

In a true culture of innovation, a leader leads the team in the new direction and leads senior management through the change in plans. Managers, who are destined to fail, try to manage expectations while the team does what it can to serve multiple gods. This situation happens so often it should have its own name. 7. Build a Yellow Brick Road

Digital transformation requires all kinds of partnerships. Some will be with old partners, some will be with frenemies, some will be with organizations you could never imagine being partners with. No matter what you call the new form of your digitally transformed organization, it will be based on an extensible platform strategy, and it will empower partners to add value in myriad ways you would never have thought of, or could ever have had time or resources to create.

To facilitate this part of your digital transformation, you will need to build a Yellow Brick Road that leads directly to your door. For example, the Yellow Brick Road for higher education leads to Harvard. The Yellow Brick Road for technology leads to Silicon Valley. Movies … Hollywood. Advertising … Madison Avenue. Finance … Wall Street. Build a Yellow Brick Road to your organization and the world’s best and brightest will follow it straight to you.

Adapt or Die!

You can take your time, but understand that today you are experiencing the slowest rate of technological change you will ever experience for the rest of your life. You really don’t have time to wait. Digital transformation will not get cheaper to do and it will not get faster to do.

This is the part where you push back and say, “Technology gets faster and cheaper and is doing so at an accelerating rate – that’s why we have to digitally transform. We can wait until we are ready or until we are forced to do it.”

While everything in the preceding quote is true, the inherent problem is that it will not only be true for you, it will be true for all of your competitors and every startup that’s gunning for a piece of your world. By then, it will be too late. Remember your Darwin: “It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is the most adaptable to change.” In other words, adapt or die!

Oxford University researchers have estimated that 47 percent of U.S. jobs could be automated within the next two decades. But which white-collar jobs will robots take first?

First, we should define “robots” (for this article only) as technologies, such as machine learning algorithms running on purpose-built computer platforms, that have been trained to perform tasks that currently require humans to perform.

With this in mind, let’s think about what you’ll do after white-collar work. Oh, and I do have a solution for the short term that will make you the last to lose your job to a robot, but I’m saving it for the end of the article.

1 – Middle Management

If your main job function is taking a number from one box in Excel and putting it in another box in Excel and writing a narrative about how the number got from place to place, robots are knocking at your door. Any job where your “special and unique” knowledge of the industry is applied to divine a causal relationship between numbers in a matrix is going to be replaced first. Be ready.

2 – Commodity Salespeople (Ad Sales, Supplies, etc.)

Unless you sell dreams or magic or negotiate using special perks, bribes or other valuable add-ons that have nothing to do with specifications, price and availability, start thinking about your next gig. Machines can take so much cost out of any sales process (request for proposal, quotation, order and fulfillment system), it is the fiduciary responsibility of your CEO and the board to hire robots. You’re fighting gravity … get out!

Writing is tough. But not report writing. Machines can be taught to read data, pattern match images or video, or analyze almost any kind of research materials and create a very readable (or announceable) writing. Text-to-speech systems are evolving so quickly and sound so realistic, I expect both play-by-play and color commentators to be put out of work relatively soon – to say nothing about the numbered days of sports or financial writers. You know that great American novel you’ve been planning to write? Start now, before the machines take a creative writing class.

4 – Accountants & Bookkeepers

Data processing probably created more jobs than it eliminated, but machine learning–based accountants and bookkeepers will be so much better than their human counterparts, you’re going to want to use the machines. Robo-accounting is in its infancy, but it’s awesome at dealing with accounts payable and receivable, inventory control, auditing and several other accounting functions that humans used to be needed to do. Big Four auditing is in for a big shake-up, very soon.

5 – Doctors

This may be one of the only guaranteed positive outcomes of robots’ taking human jobs. The current world population of 7.3 billion is expected to reach 8.5 billion by 2030, 9.7 billion in 2050 and 11.2 billion in 2100, according to a new UN DESA (United Nations Department of Economic and Social Affairs) report. In practice, if everyone who ever wanted to be a doctor became one, we still would not have enough doctors.

The good news is that robots make amazing doctors, diagnosticians and surgeons. According to Memorial Sloan Kettering Cancer Center, IBM’s Watson is teaming up with a dozen US hospitals to offer advice on the best treatments for a range of cancer, and also helping to spot early-stage skin cancers. And ultra-precise robo-surgeons are currently used for everything from knee replacement surgery to vision correction. This trend is continuing at an incredible pace. I’m not sure how robodoc bedside manner will be, but you could program a “Be warm and fuzzy” algorithm and the robodoc would act warm and fuzzy. (Maybe I can get someone to program my human doctors with a warm and fuzzy algorithm?)

But Very Few Jobs Are Safe

During the Obama administration, a report of the president was published (it is no longer available at whitehouse.gov, but here’s the original link) that included a very dire prediction: “There is an 83% chance that workers who earn $20 an hour or less could have their jobs replaced by robots in the next five years. Those in the $40 an hour pay range face a 31% chance of having their jobs taken over by the machines.” Clearly, the robots are coming.

What to Do About It

In What Will You Do After White-Collar Work?, I propose, “First, technological progress is neither good nor bad; it just is. There’s no point in worrying about it, and there is certainly no point trying to add some narrative about the “good ol’ days.” It won’t help anyone. The good news is that we know what’s coming. All we have to do is adapt.

Adapting to this change is going to require us to understand how man-machine partnerships are going to evolve. This is tricky, but not impossible. We know that machine learning is going to be used to automate many, if not most, low-level cognitive tasks. Our goal is to use our high-level cognitive ability to anticipate what parts of our work will be fully automated and what parts of our work will be so hard for machines to do that man-machine partnership is the most practical approach.

With that strategy, we can work on adapting our skills to become better than our peers at leveraging man-machine partnerships. We’ve always been tool-users; now we will become tool-partners.”

Becoming a great man-machine partner team will not save every job, but it is a clear pathway to prolonging your current career while you figure out what your job must evolve into in order to continue to transfer the value of your personal intellectual property into wealth.

Both previous essays are about robots replacing human workers who do cognitive nonrepetitive work (such as middle managers, salespersons, tax accountants, and report writers) that most people do not believe robots will be able to do any time soon. For those essays, I defined robots as technologies, such as machine learning algorithms running on purpose-built computer platforms, that have been trained to perform tasks that currently require humans to perform.

For this writing, let’s expand the definition of robot to any autonomous system designed to do work that used to require humans to perform. And let’s expand our thought experiment to include all four major categories of human tasks: Manual repetitive (predictable), Manual nonrepetitive (not predictable), Cognitive repetitive (predictable), Cognitive nonrepetitive (not predictable). In other words, let’s look at some probable futures of the real world and see where our conclusions lead us.

Joe Driver

Before being made eligible for assistance under the Universal Minimum Guaranteed Income Program Act of 2021 (also known as the “U-Min” bill, which guarantees workers displaced by robots a living wage), Joe was a professional driver.

Wait! Full Stop! Way Too Easy

Agreed. A huge number of transportation industry professionals will be replaced by autonomous vehicles, and so will dispatchers, warehouse workers and the managers who manage them. That is the easy part.

For our thought experiment, let’s replace just 20 percent of taxi, car service and truck drivers with autonomous vehicles. Now, let’s think about the businesses that service these workers. The local deli where the drivers used to stop for coffee. The attached convenience store that enables the gas station owner to run a profitable business (because there’s not enough margin in selling gas alone). The quick-serve restaurants, the supermarkets, etc. Let’s try to imagine a world where just 20 percent of transportation industry workers were laid off. Could the businesses that rely on these transportation workers survive the commensurate permanent decline in revenue?

“This is nonsense,” you say. “These people will be retrained or find other jobs.” I don’t think so, but let’s assume you are right.

The other jobs (whatever they may be) will have completely different traffic patterns (no pun intended). New behaviors will emerge and the impact of this massive behavior change will be about as pleasant as when the big box stores came to town and literally killed every mom-and-pop retail store on Main Street. Town survived, but it has never looked, felt or been the same.

In practice, this is just the soundbite version of Robot Apocalypse. Let’s go deeper.

Joe Executive

Before qualifying for subsidies under U-Min, Joe was a CPA and a tax auditing partner at a Big Four accounting firm. With more than 15 years of experience working with some of the biggest corporations in the world, his entire department was replaced by AlphaAudit from Google’s DeepMind group. Interestingly, every partner in Joe’s practice area was earning more than $450,000 per year. Some were making north of $2.1 million per year. What will they do now? Where do you take 15–25 years of accounting experience and use it in a nonaccounting job?

FOMO, “Fear of Missing Out”

If you’re wondering about the driving force behind the Robot Apocalypse, it’s FOMO, “fear of missing out.” Making the converging trends of on-demand behavior, machine learning and autonomy actionable has gone from talking points to 40 percent of our business in under two years. All of our consulting clients are rushing to put autonomous systems and machine learning tools to work. It’s not that AI systems are “plug ’n’ play” – they are far from it. But I don’t know even one CEO who wants to wake up one morning to the news that a competitor has deployed an automated system that enabled a newsworthy increase in EBITDA. In a corporate world driven by earnings calls, that would be considered a very bad day.

Which Leads Us to … Life After the Robot Apocalypse

For this imperfect guessing game about the future, let’s take some real world financial statistics to benchmark the apocalypse.

The Tax Base of the United States of America

According to an article on marketwatch.com, “An estimated 45.3% of American households — roughly 77.5 million — will pay no federal individual income tax.” The article goes on to say, “The top 1% of Americans, who have an average income of more than $2.1 million, pay 43.6% of all the federal individual income tax in the U.S.”

So, what would life be like if 20 percent of the one percent of Americans who pay 43.6 percent of all the federal individual income tax in the United States lost their jobs to robots?

The Spectrum of Probable Futures

On one extreme end of the spectrum are common post-apocalyptic themes such as spotty power, energy shortages, food shortages, no running water, nonfunctioning schools, limited resources, reduced or nonexistent healthcare, etc. I don’t think this is where we’re headed.

On the other extreme end of the spectrum is “Robotopia,” a place where humans have more time to do leisure activities, be creative, live life to the fullest, eat gourmet food, drink exotic vintage wines and spirits, practice the arts, and live under the protection of a master artificial intelligence, free from disease, free from fear, free from war … heaven on earth. I don’t think this is where we’re headed either.

Somewhere in between these two extreme views of life after the Robot Apocalypse is where we are probably going find ourselves. It’s a world where the tax base has been severely impacted by the redistribution of workers. Wizened, experienced, lifelong professionals are going to find themselves in a new world that has no interest in them. New jobs will be created in industries that do not yet exist. And the physical world will be continuously adapted and optimized to favor autonomous systems that reduce cost, improve efficacy and increase productivity.

This Is Going to Be a Huge Struggle

Will we need my hypothetical, Universal Minimum Guaranteed Income Program Act of 2021? We might. Questions like “If we all lose our jobs, who will buy the goods that the robots produce?” are good ones. We won’t all lose our jobs, but a significant percentage of people will and, in the process, be rendered unemployable.

That said, one friend of mine, who is a renowned public policy expert in D.C., told me that nothing was going to happen because we already have a nontaxpaying population explosion that is completely out of control. He opined that public assistance programs will simply continue to increase until no one except the top .05 percent of wage earners pays for anything.

The Time for Policy Innovation Is Now

It’s time for policymakers to approach policy innovation the way our corporate clients are approaching their own digital transformations. As I’ve been saying for years, today we are experiencing the slowest rate of technological change we will ever experience for the rest of our lives. The pace of technological progress is not going to slow down, ever! FOMO is a powerful force that will continue to drive innovation. We get to choose what life after the Robot Apocalypse will be like. Let’s choose wisely.

Professional poker player Jason Les plays against "Libratus," at Rivers Casino in Pittsburgh, on January 11, 2017.Andrew Rush/Pittsburgh Post-Gazette/AP

Another game just fell to the machines.

Yesterday, after 20 days of play at a casino in Pittsburgh, an AI built by two Carnegie Mellon researchers officially defeated four top players at no-limit Texas Hold ‘Em—a particularly complex form of poker that relies heavily on longterm betting strategies and game theory. Over the past twenty years, machines have topped the best humans at checkers, chess, Scrabble, Jeopardy!, and even the ancient game of Go. But no AI had ever beaten the best at such an extreme game of “imperfect information,” a game where certain elements, such as the cards on the table, are hidden. Among humans, no-limit Hold ‘Em requires a certain degree of intuition, not to mention luck.

‘We’re playing against each other. But we’re also trying to win for the humans.’

Carnegie Mellon professor Tuomas Sandholm and grad student Noam Brown designed the AI, which they call Libratus, Latin for “balance.” Almost two years ago, the pair challenged some top human players with a similar AI and lost. But this time, they won handily: Across 20 days of play, Libratus topped its four human competitors by more than $1.7 million, and all four humans finished with a negative number of chips.

Yes, poker is just a game. But the game theory exhibited by Libratus could help with everything from financial trading to political negotiations to auctions, says University of Michigan professor Michael Wellman, who specializes in game theory and closely follows the world of AI poker. In no-limit Hold ‘Em, players aren’t necessarily trying to win each small hand. They’re trying to win the most money, and that means developing betting strategies that play out over dozens of hands. A machine that masters no-limit Texas Hold ‘Em mimics the kind of human intuition these strategies require.

According to the human players that lost out to the machine, Libratus is aptly named. It does a little bit of everything well: knowing when to bluff and when to bet low with very good cards, as well as when to change its bets just to thrown off the competition. “It splits its bets into three, four, five different sizes,” says Daniel McAulay, 26, one of the players bested by the machine. “No human has the ability to do that.”

So far, Sandholm has been coy about the particulars of how Libratus operates, but he has promised to share details in the days to come. The human players—who along with McAulay include Dong Kim, Jason Les, and Jimmy Chou—believe that the machine’s play changed from day to day. If they ever felt they’d found a hole in its strategy, the hole would close. “It seemed to learn what we were doing and exploit it,” McAuley said. Sandholm and Brown may have worked to change the machine’s behavior from day to day, as they did when their earlier AI, Claudiro, went up against human players nearly two years ago. But the machine may also have learned from the match as it played out.

If it seems unfair that the Carnegie Mellon researchers may have altered the machine between rounds, consider that the human players also used every tactic at their disposal. Though the game was heads-up Hold ‘Em—meaning each player was playing his own game against the machine—they would share strategies in the evenings. “We spend a couple of hours conferring every night,” McAuley said. “We’re playing against each other. But we’re also trying to win for the humans.”

To view links or images in signatures your post count must be 15 or greater. You currently have 0 posts.

Nikita Khrushchev:"We will bury you"

"Your grandchildren will live under communism."

“You Americans are so gullible.

No, you won’t accept To view links or images in signatures your post count must be 15 or greater. You currently have 0 posts. outright, but we’ll keep feeding you small doses of To view links or images in signatures your post count must be 15 or greater. You currently have 0 posts. until you’ll finally wake up and find you already have communism.

To view links or images in signatures your post count must be 15 or greater. You currently have 0 posts. ."

We’ll so weaken your To view links or images in signatures your post count must be 15 or greater. You currently have 0 posts. until you’ll To view links or images in signatures your post count must be 15 or greater. You currently have 0 posts. like overripe fruit into our hands."

The state's comptroller has said the state is in "massive crisis mode."

June 29, 2017

The clock is ticking on the state of Illinois to pull together its first state budget in three years – but more structural fixes will be needed to resolve a multi-billion dollar debt crisis that threatens to make it the first state to be slapped with a "junk" credit rating.

For the third year in a row, the Prairie State is creeping up on its July 1 budget deadline without much progress on the financial front. The state government has continued to operate through appropriations and court orders, effectively allocating funds to schools, pensions and public entities. Pundits have taken to calling it the "Venezuela of the Midwest."

Government spending has essentially been running on "autopilot" for the past two years, says Diana Rickert, vice president of communications at the Illinois Policy Institute.

"Even without a state budget, almost all of state spending is still going on. Almost 90 percent of state spending is going on without a budget," she says.

But funding is tight, and the state has been running an annual deficit for years, effectively ballooning its debt burden. Should state officials fail to get a longer-term fix ironed out by Saturday – which is looking increasingly likely with every passing day – it would throw Illinois into uncharted waters.

"Illinois is just unique here. The prospect of going three straight years in modern times is something that we haven't seen any other state do," says John Hicks, executive director of the National Association of State Budget Officers.

Hicks notes states like Pennsylvania, Minnesota and Tennessee have also reached some kind of budgetary impasse at one point or another in the past, which were all eventually sorted out internally. But no state has gone three consecutive years without a formal budgetary road map in recent history.

Illinois Comptroller Susana Mendoza has described the state as being in "massive crisis mode" as she attempts to prioritize which bills get paid in absence of a budget plan. Earlier this month, she warned that a slew of recent court orders mandating that the state pay certain debt holders will completely exhaust the state's discretionary spending, which includes tax dollars typically funneled to, among other things, domestic violence shelters and ambulance services.

"The magic tricks run out after a while, and that's where we're at," she said in mid-June, according to The Associated Press.

Credit ranking outfits like S&P and Moody's are expected to slap Illinois with a "junk" credit rating should it fail to produce a budget by the state's July 1 deadline. S&P analyst Gabriel Petek wrote earlier this month that the state is "at risk of entering a negative credit spiral … further exacerbating its fiscal distress" when his ratings outfit downgraded Illinois from triple-B status to triple-B-minus – one step above "junk." The lower rating means it will cost money to raise debt to run the state and limit its options when it comes to lenders.

Hicks says a junk status would "have a continued effect on their cost of borrowing in Illinois." With more government money tied up in interest payments, less money is expected to be available to support programs and projects that benefit taxpayers.

And demographics aren't exactly on the state's side to bring in more government revenues. Temporary tax increases to help cover debt and pension payments expired at the end of 2014, and the number of workers employed throughout the state in May – contributing income taxes to the state's coffers – was more than 125,000 smaller than it was 10 years ago.

"Illinois has shrunk three years in a row. We used to have 26 representatives in Congress. We're predicted to have 16 in a couple of years. That's what's happening to the population," says Ted Dabrowski, vice president of policy and a spokesman at the Illinois Policy Institute.

The institute found the size of the Illinois labor force has contracted by 230,000 since the Great Recession hit in 2007. And data from The Pew Charitable Trusts suggests personal income growth in Illinois has been among the worst in the nation in recent years.

"The context is we are in the third-longest economic recovery in modern history, and Illinois' indicators are not reflecting that expansion," says Barb Rosewicz, research director at the Pew Trusts. "This is a time traditionally during an economic recovery when states would be setting aside funds to put into their reserves in anticipation of whenever the next economic downturn comes, which will be inevitable. But because of the Illinois budget problem, it has not been able to replenish its rainy day funds at all, which puts it in a vulnerable position in the event of a broader economic downturn nationally."

Indeed, the absence of a long-term budget plan also has done nothing for the state's $15 billion debt burden and rapidly escalating pension obligations. Even an eleventh-hour budget fix isn't expected to completely patch the state's financial troubles.

"Just because you don't do something for two years doesn't put you at a junk bond rating. That's not the issue. The last two years are really a culmination of about three decades of mess," Dabrowski says.

Dabrowski and Rickert place the blame at the feet of a Democratic party that at times in recent decades ran "unchecked" with a supermajority in the Illinois House and Senate. Legislation wasn't passed when Democrats called all of the shots that would have alleviated the state's growing pension problem or rein in escalating debt – aside from a temporary tax increase passed in 2010 that did not fully resolve the state's problems.

And now that the supermajority is gone and Republican Gov. Bruce Rauner is in place to oppose Democratic House Speaker Michael Madigan, the negotiation of bills that could help the state's debt situation has become complicated.

"[W]hen [Rauner] came in, he refused to sign on to what Madigan wanted, and it was really the first time someone had taken him on in decades, so that's where this gridlock really started," says Dabrowski. "So now, you get to where we are today, and you've got a pension system that's eating up a quarter of the budget now. It's eating into everything, from education to social services to higher ed to roads. And you have these unpaid bills that keep going up."

Dabrowski's and Rickert's Illinois Policy Institute as of 2013 had received roughly $500,000 in donations from Rauner, according to the Springfield State Journal-Register and Reuters.

Pension problems are not unique to Illinois, though. Eileen Norcross, a senior research fellow at George Mason University's Mercatus Center who helps direct its state fiscal rankings, says states like Illinois, Kentucky, Connecticut and New Jersey are among several that are beleaguered by pension obligations and unpaid debt.

But she says the situation in Illinois is further complicated by a provision in its state constitution that essentially prevents the government from doing anything that would result in "diminished or impaired" pensions.

"That pretty much ties their hands. They can't change benefit formulas going forward for their employees," she says. "They've built a house that is so rigid on very weak foundation, so there's no give. It's been built by politics and fiscal institutions that are really poor."

How the state moves forward from here is complicated. Under current law, states can't file for bankruptcy like Detroit, for example, so Illinois will likely have to dig itself out of its debt and pension hole. There's a general consensus among analysts, though, that a quick budget fix for fiscal year 2018 won't be enough to completely turn the Illinois debt and pension problems around.

"[E]ven once they get through this, it doesn't mean that all of their problems are solved. They have to figure out how to get through their pension debt and prepare themselves for future circumstances," says Rosewicz. "This would be an important first step, but they still have important challenges."

Illinois economically collapsing while the talking heads are busy spinning Russia-Trump collusion conspiracy theories.

Washington’s Lottery will suspend all operations if lawmakers can’t pass the state’s operating budget by midnight on Friday, June 30, 2017.

That means no Lottery tickets will be sold, and no winning tickets will be redeemed in the state of Washington for any game until the shutdown is over.

This includes Scratch games, jackpot games and multi-state jackpot games such as Powerball and Mega Millions.

Washington’s Lottery will also not conduct any jackpot game drawings during the shutdown period. This includes drawings for Match 4, Daily Game, Daily Keno, Lotto or Hit 5.

During suspended operations, players who have a winning ticket should sign the back of the ticket and keep it in a secure location. Once Washington’s Lottery services are restored, players will be able to redeem winning tickets.

The Lottery is just one of many state-run programs that will be suspended if a budget deal isn’t reached.

Notices went out last week to about 32,000 state workers warning them they will be temporarily laid off if a budget is not in place by the deadline. A partial shutdown would affect everything from community supervision of offenders on probation, to meal services to the elderly to reservations made at state parks.

“We all wish that we could have been done a long time ago,” Robinson said. “It simply is a matter of the challenge of building an operating budget and all of the policy and working of funding K-12.”

State Government Shutdown

Washington lawmakers are preparing to be briefed Thursday on details of a bipartisan compromise on a two-year state operating budget as staffers race to finish the lengthy bill.

Legislative leaders had initially said that the budget and other related documents would be posted publicly at noon Thursday, but later had to amend that, saying they won't be available until Thursday night. Democratic Rep. June Robinson, who has been part of the budget negotiations, said that exhausted staffers are trying to get the complicated bill done as quickly as possible in time for a vote Friday.

"It's an incredibly complex document to put together," she said. "We want to make sure that what we put out is accurate. They are working as fast as they possibly can."

The Democratic-controlled House and Republican-led Senate have been struggling for months to find a compromise on a budget that addresses a state Supreme Court mandate on education funding. They reached agreement on the budget after overnight negotiations that ended Wednesday morning. They are in the midst of a third overtime session, and if a new budget isn't signed into law by midnight Friday, a partial shutdown starts Saturday.

A federal judge on Friday ordered Illinois to start paying $293 million in state money toward Medicaid bills every month and an additional $1 billion over the course of the next year, worsening a cash-flow problem caused by two years of budget-free spending by state government.

U.S. District Judge Joan Lefkow's ruling came after lawyers representing Medicaid patients and attorneys for the state were unable to agree on a plan to deal with bills and pay down a $3 billion backlog owed to health care providers.

The ruling requires the state to start promptly paying all new Medicaid bills, which is estimated at about $586 million per month, and to pay down $2 billion of its bill backlog in payments spread out over the course of the coming fiscal year. The federal government pays half of those costs, so the bottom line for the state will be $293 million per month and $1 billion in backlogged bill payments over the next year.

Comptroller Susana Mendoza's office earlier in the week had offered to pay an additional $150 million per month, but the plaintiffs rejected it, saying it wasn't enough. The $150 million would have only cost the state $75 million because of the federal match, and Mendoza's office said that was all the state could spare while meeting other demands.

Now, Mendoza said Friday's ruling would cause her to likely have to cut payments to the state's pension funds, state payroll or payments to local governments. Payments to bond holders won't be interrupted, she said.

"As if the governor and legislators needed any more reason to compromise and settle on a comprehensive budget plan immediately, Friday's ruling by the U.S. District Court takes the state's finances from horrific to catastrophic," Mendoza said in a statement. "A comprehensive budget plan must be passed immediately."

In court arguments Wednesday, patients' attorney David Chizewer likened the situation to a misbehaving child provoking a frustrated parent.

"What they secretly want is for the parent to step in and stop the behavior," Chizewer said. "I think the state is asking the court to step in."

Lefkow stepped in two years ago, when Illinois' budget impasse began, and ordered the state to continue making payments to managed care organizations under Medicaid, a state and federal program that provides health care to poor people. The decision was one of many court orders that helped allow the state to continue operating for two years, and spend far beyond its means, without a formal budget in place.

As the impasse continued, bills at the comptroller's office have piled up, reaching nearly $15 billion. The Medicaid bills that Lefkow ordered to be paid have taken a backseat to other state obligations, including public employee payroll, contributions to state pension systems, distributions to local governments, state aid for elementary and high schools, and payments on state debt.

Mendoza's office has argued those payments are part of its "core priority" category. Each is either required by a state court order or written into state law. In recent weeks, the comptroller has warned that the state doesn't even have adequate cash flow to make those payments and will be at least $185 million short by August.

Earlier this month, Lefkow decided it was reasonable for Medicaid providers to expect their bills to be paid, if not in full, then enough to maintain patients' access to care. The judge ordered the two sides to negotiate a payment plan. At the time, the pile of bills owed to providers was estimated at $2 billion. Now Mendoza's office says it's more like $3 billion.

Talks broke down, however, and the lawyers representing Medicaid patients went back to court to ask the judge to compel the state to start making about $1 billion in monthly payments. When reimbursements from the federal government are factored in, the payments would put a roughly $550 million dent in the state's checking account each month.

Lawyers for the state also argued that while the bill backlog is a problem, there wasn't evidence to show that Medicaid patients had been denied care as a result.

Lefkow said she was bothered that "other people who are not as needy as these people are getting 100 percent" payment of their bills. Lefkow said she wasn't in favor of depriving workers of their salaries or skipping pension payments, but said the state "has a real problem explaining" how some people are being paid while others are not.

Lefkow said it was "obvious" the state was failing to comply with her court order to pay the Medicaid bills. But she wanted evidence of harm that's been caused to Medicaid patients as a result. She ordered the lawyers for the patients to submit affidavits documenting the damage.

The average net charge-off rate for large U.S. card issuers rose to 3.29% in Q2, its highest level in four years and the fifth consecutive quarter of Y/Y increases, Fitch Ratings reports.

All eight of the largest issuers - JPMorgan Chase (NYSE:JPM), Citigroup (NYSE:C), CapitalOne (NYSE:COF), Discover (NYSEFS), U.S. Bank (NYSE:USB), Wells Fargo (NYSE:WFC), Bank of America (NYSE:BAC) and American Express (NYSE:AXP) - saw increases for the quarter.

“The overall environment is deteriorating,” DFS CEO David Nelms tells WSJ, noting the new string of losses in the industry after 24 quarters of declines.

The trend of losses is occurring even amid near-record lows in U.S. unemployment, raising fears that credit performance could quickly weaken if the jobs situation weakens.

“We’ve seen an inflection point in credit,” says Charles Peabody, managing director at Compass Point Research & Trading. “It is going to get worse from here."

The total costs of Social Security will exceed total income this year for the first time since 1982, according to the annual Social Security and Medicare trustees report released on Tuesday, as funds for Medicare are expected to run dry earlier than expected.

While costs have exceeded net income since 2010, this is the first time in more than three decades that spending is expected to outweigh total income, by about $2 billion, meaning asset reserves will decline. Asset reserves as of 2017 were $2.9 trillion.

The trustees forecast that 100% of benefits will be covered through 2034, after which the trust funds for Social Security, which also cover old age and disability insurance programs, will only be able to cover about 79% of benefits.

Meanwhile, Medicare’s hospital insurance trust fund is expected to run dry in 2026, three years earlier than what the trustees had predicted in last year’s report. At that time, funds will be sufficient to cover just 91% of Medicare Part A costs.

Challenges for both programs are exacerbated by the aging of the baby boomer population, without an equivalent proportion of workers available to replace them in the workforce.

Despite looming shortfalls, U.S. Treasury Secretary Steven Mnuchin said accelerated economic growth under the current administration would help to bolster both programs’ coffers in the coming years.

“The administration’s economic agenda – tax cuts, regulatory reform, and improved trade agreements – will generate the long-term growth needed to help secure these programs and lead them to a more stable path,” Mnuchin said in a statement on Tuesday.

Sixty-two million people, including 45 million retired workers, were receiving OASDI benefits at the end of 2017. Social Security and Medicare account for 42% of all federal spending.

They will never cut benefits for Social Security. It would be a revolution the next day.

That said...

I can get SS in 2034. If it means I get 21% less getting it in 2035, I'll get it early. Maybe I should apply as early as I can and ride it out before the haircut comes.

"Far better it is to dare mighty things, to win glorious triumphs even though checkered by failure, than to rank with those poor spirits who neither enjoy nor suffer much because they live in the gray twilight that knows neither victory nor defeat."

-- Theodore Roosevelt

They will never cut benefits for Social Security. It would be a revolution the next day.

That said...

I can get SS in 2034. If it means I get 21% less getting it in 2035, I'll get it early. Maybe I should apply as early as I can and ride it out before the haircut comes.

I don't consider SS as anything more than an unwanted deduction on my paycheck. It doesn't factor at all into my retirement because I'm sure I'll never see any of it.

Like you said, they'll never cut SS benefits. I'll go a degree further in clarification... They'll never cut benefits for those already collecting them or very close. What they'll likely do to preserve it is cut it off for folks around my age and younger (likely via strict means testing) and say, "Thanks for your contribution but hope you were contributing to your 401k too!", while still forcing us to contribute. They'll "fix the glitch" for current recipients and kick the can down the road for us since we'll be a future politician's problem.

That or, because of the huge amount of money sitting in 401ks, they'll appropriate that and fold it into SS.

Will probably depend if an R or D is in office as to which one we get.

ETA: From the ARFCOM discussion on the topic...

I think I've discovered my new retirement game plan!

The profound question which transcends all this day-to-day market drama over the holidays is the nature of the economic slowdown now occurring globally. This slowdown can be seen both inside and outside the US. In reviewing the laboratory of history — especially those experiments featuring severe asset inflation, unaccompanied by high official estimates of consumer price inflation — three possible “echoes” deserve attention in coming weeks and months. (History echoes rather than repeats!)

Will We Learn from History — And What Will Soon Be History?

The behavioral finance theorists tell us that which echo sounds and which outcome occurs is more obvious in hindsight than to anyone in real time. As Daniel Kahneman writes (in Thinking Fast and Slow):

The core of hindsight bias is that we believe we understand the past, which implies the future should also be knowable; but in fact we understand the past less than we believe we do – compelling narratives foster an illusion of inevitability; but no such story can include the myriad of events that would have caused a different outcome .

Whichever historical echo turns out to be loudest as the Great Monetary Inflation of 2011-18 enters its late dangerous phase. Whether we're looking at 1927-9, 1930-3, or 1937-8, the story will seem obvious in retrospect, at least according to skilled narrators. There may be competing narratives about these events — even decades into the future, just as there still are today about each of the above mentioned episodes. Even today, the Austrian School, the Keynesians, and the monetarists, all tell very different historical narratives and the weight of evidence has not knocked out any of these competitors in the popular imagination.

The Stories We Tell Ourselves Are Important

And while on the subject of behavioral finance’s perspectives on potential historical echoes and actual market outcomes, we should consider Robert Shiller’s insights into story-telling (in “Irrational Exuberance”):

Speculative feedback loops that are in effect naturally occurring Ponzi schemes do arise from time to time without the contrivance of a fraudulent manager. Even if there is no manipulator fabricating false stories and deliberately deceiving investors in the aggregate stock market, tales about the market are everywhere….. The path of a naturally occurring Ponzi scheme – if we may call speculative bubbles that – will be more irregular and less dramatic since there is no direct manipulation but the path may sometimes resemble that of a Ponzi scheme when it is supported by naturally occurring stories.

Bottom line: great asset inflations (although the term "inflation" remains foreign to Shiller!) are populated by “naturally occurring Ponzi schemes,” with the most extreme and blatant including Dutch tulips, Tokyo golf clubs, Iceland credits, and Bitcoins; the less extreme but much more economically important episodes in recent history include financial equities in 2003-6 or the FANMGs in 2015-18; and perhaps the biggest in this cycle could yet be private equity.

Echoes of Past Crises

First, could 2019-21 feature a loud echo of 1926-8 (which in turn had echoes in 1987-9, 1998-9, and 2015-17)?

The characteristic of 1926-8 was a “Fed put” in the midst of an incipient cool-down of asset inflation (along with a growth cycle slowdown or even onset of mild recession) which succeeds apparently in igniting a fresh economic rebound and extension/intensification of asset inflation for a while longer (two years or more). In mid-1927 New York Fed Governor Benjamin Strong administered his coup de whiskey to the stock market (and to the German loan boom), notwithstanding the protest of Reichsbank President Schacht).

The conditions for such a Fed put to be successful include a still strong current of speculative story telling (the narratives have not yet become tired or even sick); the mal-investment and other forms of over-spending (including types of consumption) must not be on such a huge scale as already going into reverse; and the camouflage of leverage — so much a component of “natural Ponzi schemes” — must not yet be broken. The magicians, otherwise called “financial engineers” still hold power over market attention.

Most plausibly we have passed the stage in this cycle where such a further kiss of life could be given to asset inflation. And so we move on to the second possible echo: could this be 1937-8?

There are some similarities in background. Several years of massive QE under the Roosevelt Administration (1934-6) (not called such and due ostensibly to the monetization of massive gold inflows to the US) culminated in a stock market and commodity market bubble in 1936, to which the Fed responded by effecting a tiny rise in interest rates while clawing back QE. Under huge political pressure the Fed reversed these measures in early 1937; a weakening stock market seems to reverse. But then came the Crash of late Summer and early Autumn 1937 and the confirmed onset of the Roosevelt recession (roughly mid-1937 to mid-1938). This was even more severe than the 1929-30 downturn. But then there was a rapid re-bound.

On further consideration, there are grounds for skepticism about whether the 1937-8 episode will echo loudly in the near future.

In 1937 there had been barely three years of economic expansion. Credit bubbles and investment spending bubbles (mal-investment) were hardly to be seen. And the monetary inflation in the US was independent and very different from monetary conditions in Europe, where in fact the parallel economic downturn was very mild if even present. And of course the re-bound had much to do with military re-armament.

It is troubling that the third possible echo — that of the Great Depression of 1930-2 — could be the most likely to occur.