40 'Frightening' Facts On The Fall Of The US Economy

May 27, 2013

Submitted by Michael Snyder of The Economic Collapse blog,

40 Statistics About The Fall Of The U.S. Economy That Are Almost Too Crazy To Believe

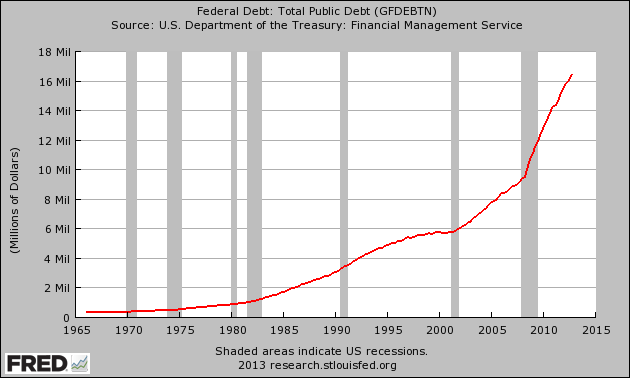

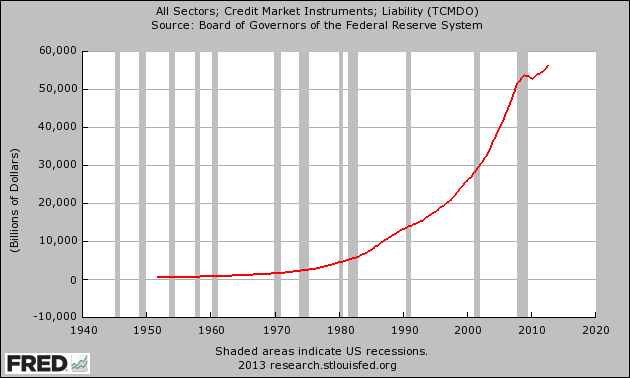

If you know someone that actually believes that the U.S. economy is in good shape, just show them the statistics in this article. When you step back and look at the long-term trends, it is undeniable what is happening to us. We are in the midst of a horrifying economic decline that is the result of decades of very bad decisions. 30 years ago, the U.S. national debt was about one trillion dollars. Today, it is almost 17 trillion dollars. 40 years ago, the total amount of debt in the United States was about 2 trillion dollars. Today, it is more than 56 trillion dollars. At the same time that we have been running up all of this debt, our economic infrastructure and our ability to produce wealth has been absolutely gutted. Since 2001, the United States has lost more than 56,000 manufacturing facilities and millions of good jobs have been shipped overseas. Our share of global GDP declined from 31.8 percent in 2001 to 21.6 percent in 2011. The percentage of Americans that are self-employed is at a record low, and the percentage of Americans that are dependent on the government is at a record high. The U.S. economy is a complete and total mess, and it is time that we faced the truth.

The following are 40 statistics about the fall of the U.S. economy that are almost too crazy to believe...

#1 Back in 1980, the U.S. national debt was

less than one trillion dollars. Today, it is rapidly approaching 17 trillion dollars...

#2

#2 During Obama's first term, the federal government accumulated more debt than it did under

the first 42 U.S presidents combined.

#3 The U.S. national debt is now

more than 23 times larger than it was when Jimmy Carter became president.

#4 If you started paying off

just the new debt that the U.S. has accumulated during the Obama administration at the rate of one dollar per second, it would take

more than 184,000 years to pay it off.

#5 The federal government is stealing more than 100 million dollars from our children and our grandchildren every single hour of every single day.

#6 Back in 1970, the total amount of debt in the United States (government debt + business debt + consumer debt, etc.) was less than 2 trillion dollars. Today it is over 56 trillion dollars...

#7

#7 According to the World Bank, U.S. GDP accounted for

31.8 percent of all global economic activity in 2001. That number dropped to

21.6 percent in 2011.

#8 The United States has fallen in the global economic competitiveness rankings compiled by the World Economic Forum

for four years in a row.

#9 According to The Economist, the United States was the best place in the world to be born into

back in 1988. Today, the United States is only

tied for 16th place.

#10 Incredibly,

more than 56,000 manufacturing facilities in the United States have been permanently shut down since 2001.

#11 There are less Americans working in manufacturing today

than there was in 1950 even though the population of the country has more than doubled since then.

#12 According to the New York Times, there are now

approximately 70,000 abandoned buildings in Detroit.

#13 When NAFTA was pushed through Congress in 1993, the United States had a trade

surplus with Mexico of 1.6 billion dollars. By 2010, we had a trade

deficit with Mexico of

61.6 billion dollars.

#14 Back in 1985, our trade deficit with China was approximately

6 million dollars (million with a little "m") for the

entire year. In 2012, our trade deficit with China was

315 billion dollars. That was the largest trade deficit that one nation has had with another nation in the history of the world.

#15 Overall, the United States has run a trade deficit of

more than 8 trillion dollars with the rest of the world since 1975.

#16 According to the Economic Policy Institute, the United States is losing

half a million jobs to China every single year.

#17 Back in 1950,

more than 80 percent of all men in the United States had jobs. Today,

less than 65 percent of all men in the United States have jobs.

#18 At this point, an astounding

53 percent of all American workers make less than $30,000 a year.

#19 Small business is rapidly dying in America. At this point,

only about 7 percent of all non-farm workers in the United States are self-employed. That is an all-time record low.

#20 Back in 1983, the bottom 95 percent of all income earners in the United States had 62 cents of debt for every dollar that they earned. By 2007, that figure had soared

to $1.48.

#21 In the United States today, the wealthiest one percent of all Americans have a greater net worth

than the bottom 90 percent combined.

#22 According to Forbes, the 400 wealthiest Americans have more wealth than the bottom 150 million Americans

combined.

#23 The six heirs of Wal-Mart founder Sam Walton have as much wealth as the bottom one-third of all Americans

combined.

#24 According to the U.S. Census Bureau,

more than 146 million Americans are either "poor" or "low income".

#25 According to the U.S. Census Bureau,

49 percent of all Americans live in a home that receives direct monetary benefits from the federal government. Back in 1983,

less than a third of all Americans lived in a home that received direct monetary benefits from the federal government.

#26 Overall, the federal government runs

nearly 80 different "means-tested welfare programs", and at this point

more than 100 million Americans are enrolled in at least one of them.

#27 Back in 1965, only one out of every 50 Americans was on Medicaid. Today,

one out of every 6 Americans is on Medicaid, and things are about to get a whole lot worse. It is being projected that Obamacare will add

16 million more Americans to the Medicaid rolls.

#28 As I wrote

recently, it is being projected that the number of Americans on Medicare will grow from 50.7 million in 2012 to

73.2 million in 2025.

#29 At this point, Medicare is facing unfunded liabilities of more than 38 trillion dollars over the next 75 years. That comes to approximately

$328,404 for every single household in the United States.

#30 Right now, there are approximately 56 million Americans collecting Social Security benefits. By 2035, that number is projected to soar to an astounding

91 million.

#31 Overall, the Social Security system is facing a

134 trillion dollar shortfall over the next 75 years.

#32 Today, the number of Americans on Social Security Disability now exceeds

the entire population of Greece, and the number of Americans on food stamps now exceeds

the entire population of Spain.

#33 According to a report recently issued

by the Pew Research Center, on average Americans over the age of 65 have 47 times as much wealth as Americans under the age of 35.

#34 U.S. families that have a head of household that is under the age of 30 have a poverty rate

of 37 percent.

#35 As I mentioned

recently, the homeownership rate in America is now at its lowest level

in nearly 18 years.

#36 There are now

20.2 million Americans that spend more than half of their incomes on housing. That represents a 46 percent increase from 2001.

#37 45 percent of all children are living in poverty in Miami,

more than 50 percent of all children are living in poverty in Cleveland, and about

60 percent of all children are living in poverty in Detroit.

#38 Today,

more than a million public school students in the United States are homeless. This is the first time that has ever happened in our history.

#39 When Barack Obama first entered the White House, about 32 million Americans were on food stamps. Now,

more than 47 million Americans are on food stamps.

#40 According

to one calculation, the number of Americans on food stamps now exceeds the combined populations of "Alaska, Arkansas, Connecticut, Delaware, District of Columbia, Hawaii, Idaho, Iowa, Kansas, Maine, Mississippi, Montana, Nebraska, Nevada, New Hampshire, New Mexico, North Dakota, Oklahoma, Oregon, Rhode Island, South Dakota, Utah, Vermont, West Virginia, and Wyoming."

Reply With Quote

Reply With Quote

Bookmarks